Program Management was Unbundled Only to be Re-bundled

Unbundling: How We Got Here

In 2018, our investors at a16z suggested that the unbundling of the Bank was driving fintech trends. From just lending, we saw breakouts into BNPL, Earned Wage Access, and a wave of student and subprime lenders. Individual Fraud, Risk, and AML solutions proliferated and are now back to consolidating. Adjacent industries like insurance and trade solutions also felt significant influence from fintech.

Payments was a corner of fintech where unbundling was particularly dramatic. Neobanks like Chime and Cash App attacked the bread-and-butter products of retail banks by offering checking and savings alternatives. Varo made history when it became the first U.S. fintech to earn a national banking license, having also received its FDIC approval for deposit insurance earlier.

Until recently, fintech issuing had discrete roles required to set up a program in the US: The Issuer Processor, the Program Manager, and the BIN Sponsor Bank. Fintechs significantly blurred these roles. Bundles of services were being created on the fly. Issuer processors rolled up program management services, and new entrants waded into Bin Sponsorship. The competition was fierce, and it felt chaotic. We are seeing some fallout now. Setting aside some of the headlines, at VGS we are seeing a clear trend - thriving fintech issuing programs are now rebundling Program Management capabilities as a la carte software solutions to create their custom issuing stack.

Card Issuance Program Managers

Card Issuance offers significant benefits for issuers, including new revenue streams, customer loyalty and retention, brand enhancement, and customer perception as a full-service provider. However, issuing a card can be complex and requires specific expertise, which involves engaging and managing multiple third-party vendors.

In the past, this is where specialized card program managers came in. One of the motivations of early Banking as a Service models was to bundle program management services together. Today, many services have unbundled and become discrete software solutions that a fintech issuer can adopt a la carte. Selecting the right stack of solutions to build an issuer program is mission-critical.

The benefit of the unbundling is that issuers can create a card issuance program that meets their unique needs. The downside is that they must manage multiple vendors.

Best Fit Program Management for Fintechs: Rebundling

While fintechs would benefit by being their own program manager, the need to hold sensitive PCI data can be a deterrent. Achieving and maintaining PCI compliance can take time and resources away from core business needs, leading many fintechs down the route of one-size-fits-all program management instead of a custom stack that fits their unique needs.

When fintechs own their own program management function, they can control and optimize it. The previous program management function gets reset as a collection of specialized software that separately covers all of the above. Scaled fintechs will benefit by owning their destiny - as in, their own Program Management Capabilities - instead of relying on a BAAS player or a traditional verticalized Program Manager.

A PCI-compliant location is needed to orchestrate discrete software services for the most effective program management outcomes. Instead of attempting to manage multiple walled gardens, issuers can use a central vault and control all the pre-and post-functions themselves. If they are already working with a vault provider, they can go beyond payment data routing to also do risk, identity, onboarding, and dispute resolution routing.

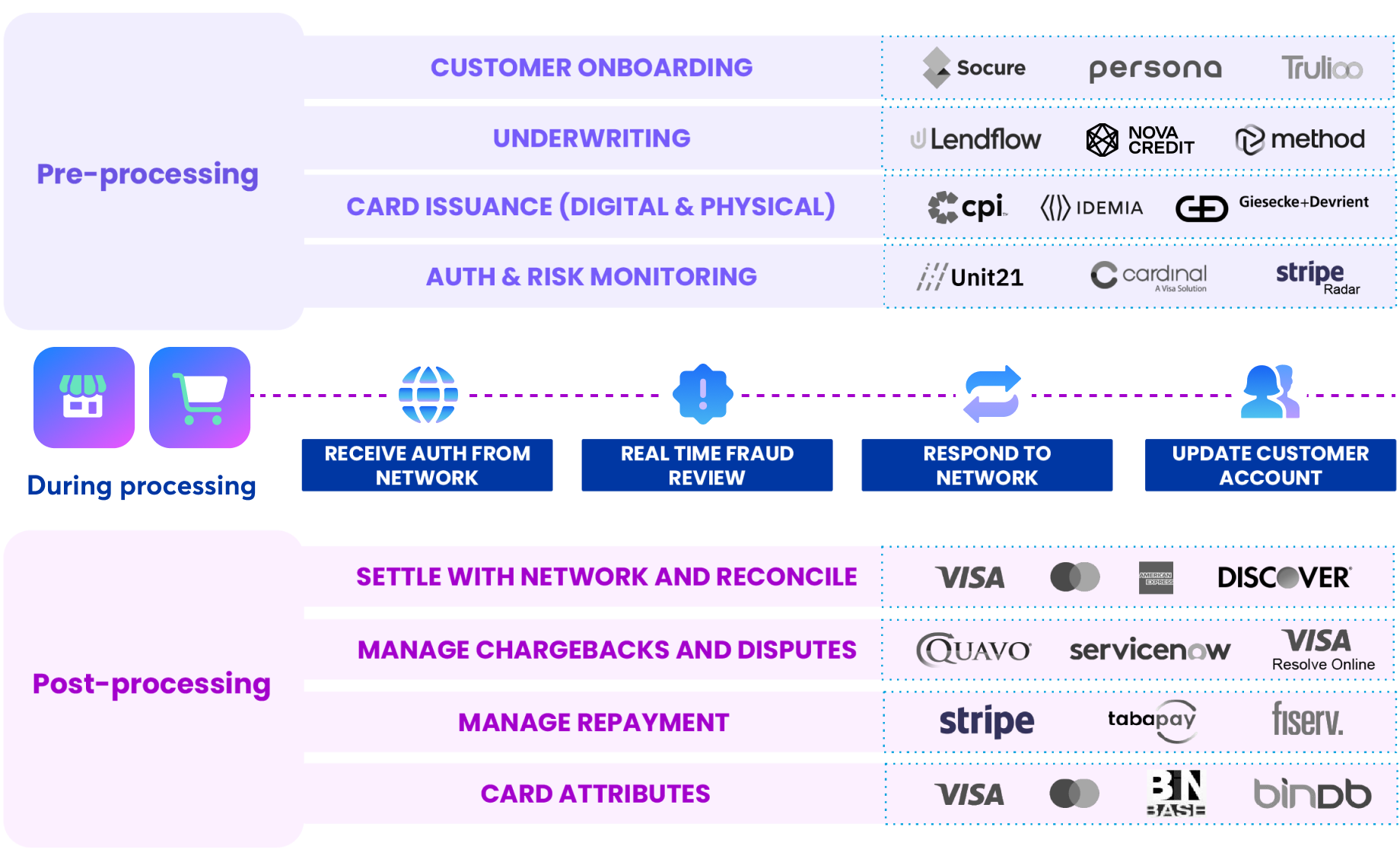

What does Program Management cover?

The critical data-centric components of program management include:

- Customer Onboarding

- Underwriting

- Card Issuance (digital and physical)

- Auth & Risk Monitoring

- Network Settlement & Reconciliation

- Chargebacks and Dispute Management

- Repayment Management

- Card Attributes Lookup

Here's a great primer on Program Management: https://www.galileo-ft.com/blog/the-essential-guide-to-payment-card-program-management/

The PCI-compliant VGS Vault offers issuers the flexibility to rebundle individual services and become their own program managers. This gives them control over their data and the providers they want to work with and the cost-effectiveness of making the decisions that best suit their needs, while not increasing their compliance requirements.

Orchestrating pre- and post-processing services requires working across multiple vendors. A separate vendor is needed for each activity, such as onboarding, underwriting, issuance, risk monitoring at the pre-stage, and settlement, chargeback resolution, and repayment management at the post-stage. All these vendors then need to be coordinated, which can be messy and time-consuming if done in a decentralized way.

Contrast this with the power of data centralization for effective program management. With a central vault, issuers can replace the effort and resources needed to manage a complex and sometimes rigid web of vendors with the ability to orchestrate them into a program management solution that best suits them as the issuer.

Are you interested in learning more about how mature fintechs and issuers leverage the VGS Vault to orchestrate program management for flexibility and centralization while maintaining PCI compliance? Contact Us.