PCI DSS Compliance Solutions for Payment Businesses

It's Easier to Focus on Growth When You Have PCI Compliance Covered

Whether you need to maintain and expand payments infrastructure without expanding your PCI footprint, are scaling your payments technology stack across businesses, or setting up a new business that requires PCI certification, VGS can help.

Achieve the requirements mandated in PCI DSS v4.0 or become PCI Compliant for the first time. The VGS Vault enables you to scale securely and rapidly with the freedom to operate on sensitive payment data without ever touching it.

Contact UsSign Up

GROW FASTER

PCI Solutions

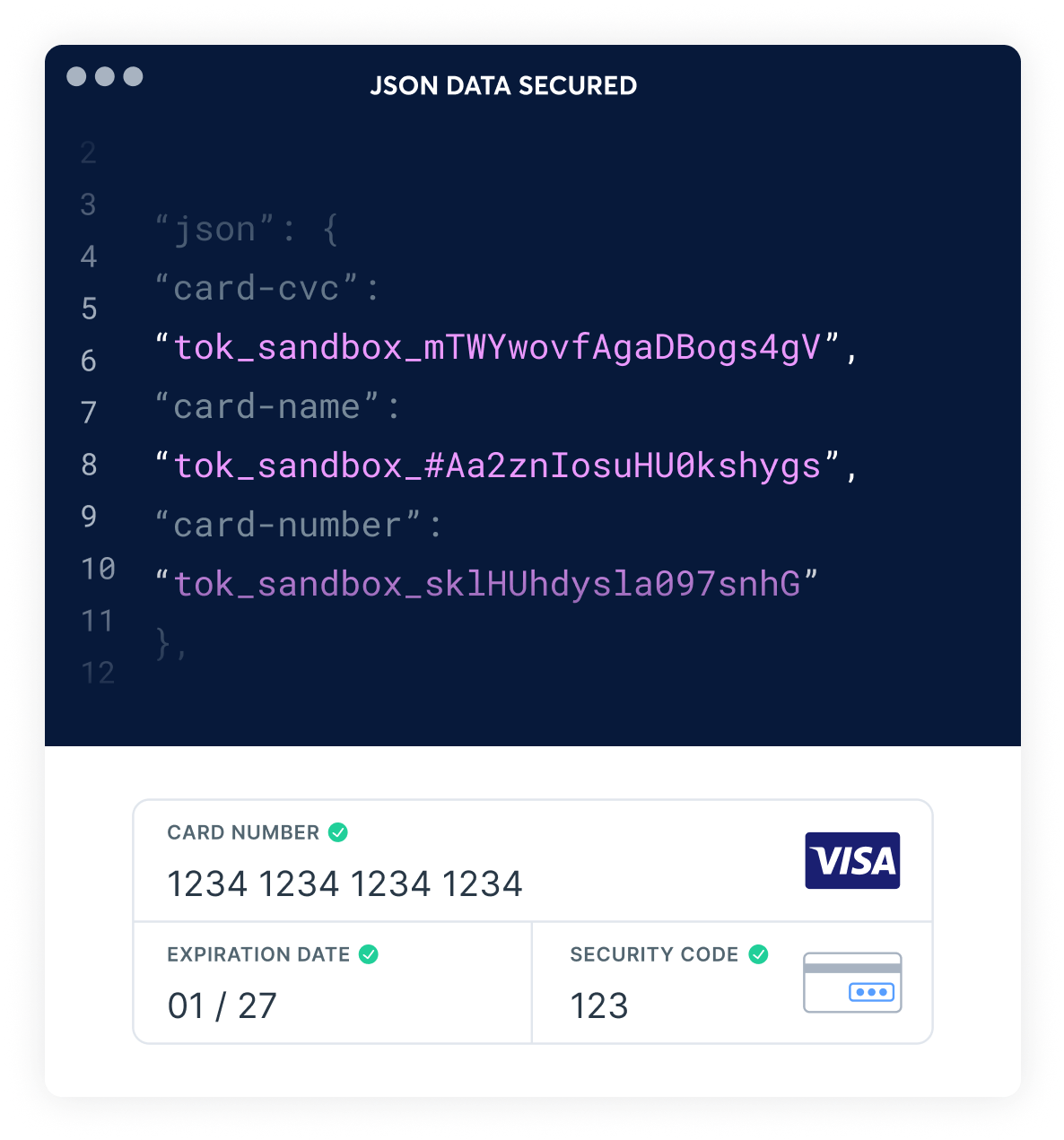

Your dedicated VGS Vault allows you to work with a broad array of payment data and not be in scope for PCI Compliance. With VGS, you can safely collect, protect, and send payment data to third-party endpoints by swapping out raw sensitive information with our secure tokens.

- Continuous PCI DSS Compliance

- Offload Liability, Risk & Burden

- Enterprise-Grade Security

- Retain Data Ownership & Portability

- Secure all types of data, including PII, PHI or Bank Credentials

MEET THE REQUIREMENTS

PC DSS v4.0 is the industry standard

PCI DSS v4.0 has been the industry standard since 2024.

PCI DSS v4.0 is the PCI standard. QSAs have already switched to conducting new PCI level 1 assessments against PCI DSS v4.0.

All the PCI DSS v4.0 future-dated requirements are mandatory.

Companies must keep their processes, procedures, and technology up-to-date to ensure that they not only set up PCI-compliant Cardholder Data Environments (CDE) and maintain them annually, but also meet the PCI DSS v4.0.

Who does PCI DSS v4.0 apply to?

Any organization that deals with Credit or Debit cardholder data.

if you,

- Store

- Transmit;

- Process; or

- Can Otherwise Affect the Security of

Sensitive Credit or Debit card data, you are subject to PCI DSS 4.0 requirements.

In other words, your cardholder data environment (CDE) is in “in-scope,” and you are subject to its guidelines.

How it Works

Descope PCI Data

As the leading PCI Tokenization Provider, our platform enables companies to process sensitive payment data without ever touching it. The VGS Solution shields you from sensitive payment data by substituting it with non-relational tokens or aliases (synthetic data) in real time. VGS operates at the network level, so your systems never come into contact with sensitive data. You stay entirely protected without any architecture changes or the need to integrate a separate API, freeing your organization to focus on growing your business rather than worrying about protecting it.

Get Continuous PCI Compliance Service

Maintain continuous PCI compliance with VGS's dedicated full-time resources, building a secure network, protecting cardholder data, enforcing information security policies, and more.

Start Descoping Now

Get Continuous PCI Compliance Service

Maintain continuous PCI compliance with VGS's dedicated full-time resources building a secure network, protecting cardholder data, enforcing information security policies, and more

Reduce Costs

Instead of wasting resources maintaining your PCI-compliant environment and consolidating data into it, or even pursuing PCI from scratch, offload your data security to VGS. Save on costs and time for compliance, and redirect your efforts to your business instead.

Maximize Data Value

Extract maximum value from your data with full format preservation and avoid vendor lock-in with complete ownership, portability, and utility of your data

Get PCI Level 1 certified in as little as 21 days

Achieving PCI Level 1 on your own often takes 6-12 months, or longer, on top of recurring annual PCI security maintenance and audits. Reaching Level 1 requires dedicated full-time resources to build and maintain a secure network, protect cardholder data, uphold a vulnerability management program, implement strong access control, monitor and test networks, and enforce an information security policy.

PCI Level 1 is achievable in just 21 days, no matter the type of business (merchant, service provider, or other). Integrate to VGS with no changes to existing systems, and instantly begin securing, managing and using sensitive data.

FAQs

Solve PCI Compliance for Good

Descope from PCI DSS and offload your compliance burden to VGS so you can focus on what matters most - growing your business.

Contact UsSign UpAI and PCI Compliance

AI systems in payment environments expand your PCI DSS scope. Learn the risks, requirements, and steps to get and stay compliant with PCI DSS 4.0 in 2026.

Learn MorePCI DSS v.4.0 is here. Are you ready?

The newest evolution of the PCI Data Security Standards (PCI DSS) is almost upon us.

Learn More