As agentic protocols, such as AP2 and MCP, reshape how digital transactions are initiated, evaluated, and completed, merchants must understand the data elements being passed through these protocols and which data they don't have access to.

From a merchant's point of view, the most dangerous part of agentic commerce and protocols is that they lose touch with their customers. When merchants can't understand how and why customers make purchases, they cannot make the most informed business decisions regarding loyalty programs, lifetime value, and even targeted promotions.

The age of agentic commerce can introduce new avenues for conversion, but it can also introduce a series of data blind spots for merchants, especially when it comes to payments and transactions.

At the core of the structured flow between users, agents, and merchants in agentic commerce are 4 essential data elements that can be identified:

- Agent identification: An agent is defined as a legitimate agent and not a bot.

- Identification and Verification of a User: A person's identity is validated, confirming that they are who they claim to be.

- Consumer Mandates: The user has authorized this purchase according to specific parameters.

- Payment Credentials: The valid payment credentials are provided to process the transaction.

-

Agent Identification

Agent identification is a crucial aspect of agentic commerce, where “agents” often resemble automated bots on a webpage. Merchants face a challenge in distinguishing between legitimate agents and malicious bots. While consumers understand that their agent is legitimate, when an agent crawls a merchant's website, the merchant has no way of knowing if the agent is, in fact, a human or a bot.

To address this, all protocols in agentic commerce include an agent registration step that essentially asks, “Who is the agent?” though each protocol handles this verification differently.

Effective agent identification must occur at multiple points:

- at the network level where agents can be provisioned with an agentic token

- and at the merchant level, where merchants can recognize and permit legitimate agents.

For example, Amazon currently blocks traffic from Perplexity because it cannot determine whether the incoming requests come from a trusted agent, demonstrating the broader need for standardized agent identification. Luckily, Cloudflare just announced a collaboration with Visa around this.

-

ID & Verification

Confirming the identity of the consumer is mandated in many markets. Even in markets where it's not mandated, CNP merchants are broadly familiar with 3DS.

One novelty of an agentic transaction is that the merchant becomes reliant on the agent to step in and verify the consumer. The merchant then becomes one level removed and doesn't have access to the consumer's identity. Merchants simply have to trust that this happened as part of the flow with the agent, but they don't receive that information directly in this flow. The merchant then cannot save the user for a future purchase or use the information for a chargeback. An example of this is when a user goes through 3DS on a merchant website; the merchant can add a 'tag' to that user to help with their own fraud detection and chargeback prevention.

That is lost in the current model.

While many protocols, such as AP2 and VIC, have considered how to transmit identity verification information to the network, there is no consensus approach on how this data flows to merchants.

-

Consumer Mandates

In agentic commerce, a consumer mandate refers to the explicit set of permissions and instructions that a consumer gives to their agent to act on their behalf.

Consumer mandates define what the agent is authorized to do, such as which merchants to engage with, what price ranges to consider, preferred payment methods, shipping preferences, or even ethical or sustainability criteria that guide purchase decisions.

Today, merchants have no visibility into these consumer preferences. They rely entirely on the agent to discover their products, build a cart, and initiate a transaction, without understanding the motivations or constraints driving the consumer's choices. This lack of insight means that merchants are often unaware of why a customer's agent selected (or ignored) their offerings, limiting their ability to optimize product presentation, pricing, or promotions.

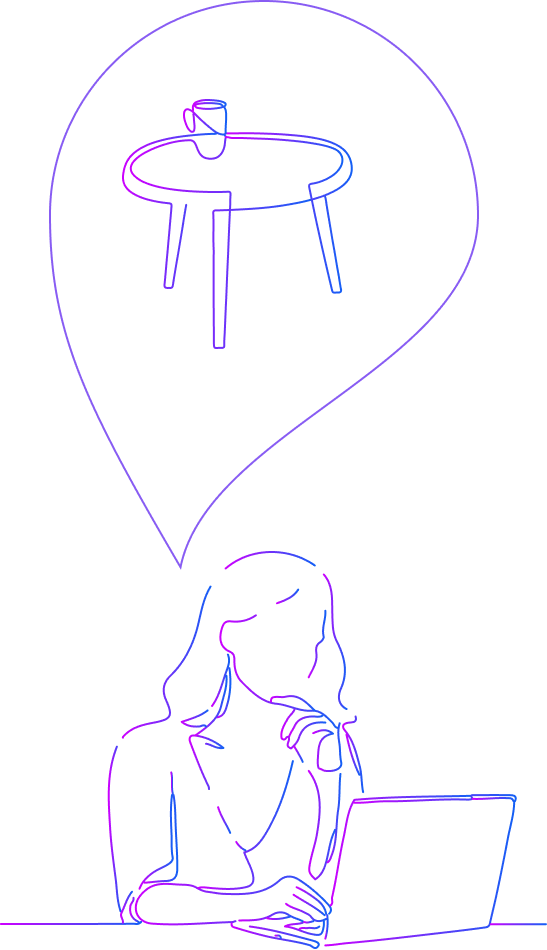

Let's look at an example of this.

A user prompts their shopping agent to purchase an end table for up to $500. A merchant happens to sell a table priced at $501.

If thousands of users have configured similar agent rules, “buy an end table under $500”, then, in theory, this merchant could convert a large volume of buyers simply by lowering their price to $499.

The problem is that, under the current agent authorization protocols and models, the merchant never receives that signal. They don't know that a massive number of agents are attempting to purchase within that range, or that they're losing conversions by a single dollar.

As a result, the merchant misses out on potentially huge margins and demand intelligence.

Ultimately, a failed authorization is the likely outcome if the agent acts outside of the mandate. However, if an agent passes this data to the merchant, they can make an informed business decision (e.g., lower their price to $499 at the time the agent is on their site).

-

Payment Credential

Once a user completes all the back-and-forth interactions with an agent, the merchant ultimately receives only an agent token (a type of network token). This token verifies that the user has successfully completed the necessary authentication and interaction steps. The token is single-use and cannot be leveraged for purposes such as loyalty programs, card-on-file storage, subscriptions, or other ongoing customer relationships.

In theory, this step could include all four data elements (agent identification, user identification, shopping preferences, and valid payment credentials); however, as the protocols currently contemplate, merchants end up with only abstracted credentials rather than all of the identifiable customer data.

This abstraction creates several challenges. The PSP can still settle the transaction, but cannot disclose the underlying customer identity or funding source. The merchant receives confirmation that payment was settled, but without any traceable lineage showing where the funds originated or which agents facilitated the transaction. As a result, dispute handling and reconciliation depend heavily on intermediaries instead of direct merchant insight.

In this model, the payment ecosystem becomes opaque for both visibility and contextual understanding for merchants and PSPs alike.

Conclusion

Without access to these data elements, merchants are forced to operate in the dark. They cannot:

- Distinguish trusted agents from malicious bots.

- Verify or tag users for future transactions.

- Interpret consumer intent or understand the rules shaping a purchase attempt.

- Connect payment credentials to meaningful customer insights, loyalty opportunities, or dispute workflows.

The result is a fragmented ecosystem where merchants are asked to trust the process without being provided with the necessary information to participate effectively.

But this gap is not a permanent condition; it's an inflection point. As standards evolve and interoperability between agents, networks, and merchant systems improves, these data elements can become the foundation for a more transparent, efficient, and collaborative commerce experience. With the right infrastructure, merchants can regain critical visibility, agents can act with greater precision and accountability, and consumers can benefit from seamless, personalized purchasing governed by their own preferences.

VGS is the merchant infrastructure solution in agentic commerce

As agentic commerce continues to evolve, shared data is becoming critical to maintaining trust and efficiency across the ecosystem.

Contact VGS to learn how we can help you.

Contact Us